Most Purchase Agreements Are Contingent on Which Two Items? A Complete Guide for Homebuyers

If you’re searching for your dream home or preparing to sell, you’ve probably come across the word “contingent” in real estate listings or during negotiations. But what does it really mean—and, more importantly, what are the two most common contingencies in a purchase agreement? At YesLoanz.com, we’re here to demystify these essential contract terms so you can move forward with confidence.

What Does “Contingent” Mean in Real Estate?

In real estate, a contingency is a condition written into the purchase agreement that must be met for the sale to proceed. If a contingency is not satisfied, the buyer (and sometimes the seller) can walk away from the deal without penalty. Think of contingencies as legal “escape hatches” that protect both parties from unforeseen problems that could otherwise result in financial loss or legal headaches.

For example, if a buyer’s offer is accepted but a home inspection reveals major issues, the buyer can back out of the deal and keep their earnest money deposit. Similarly, if the buyer can’t secure a mortgage, they aren’t forced to complete a purchase they can’t afford.

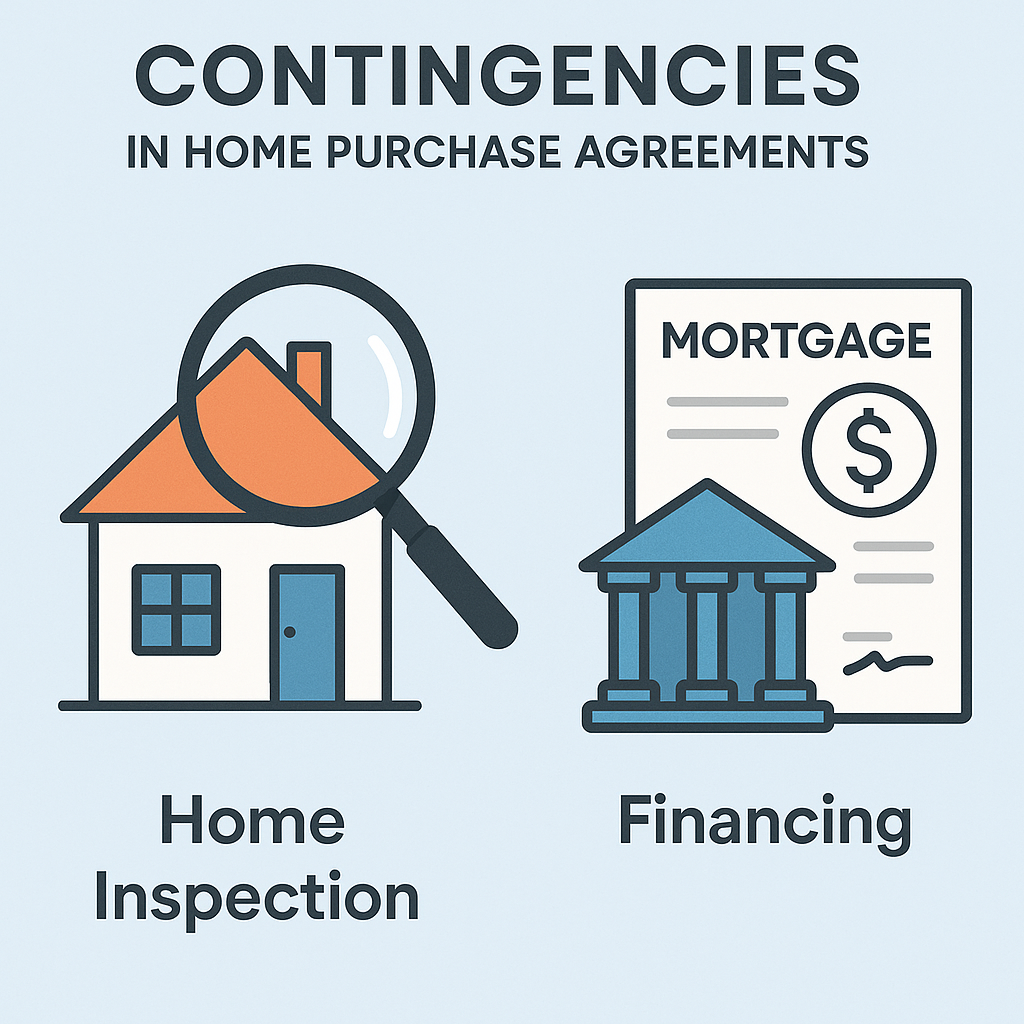

Most Purchase Agreements Are Contingent on Which Two Items?

The two most common contingencies found in home purchase agreements are:

- Home Inspection Contingency

- Financing (Mortgage) Contingency

Let’s take a closer look at each and see why they are so important for both buyers and sellers.

1. Home Inspection Contingency

What Is a Home Inspection Contingency?

A home inspection contingency gives the buyer the right to have the property professionally inspected within a specified period—usually 7 to 14 days after the contract is signed. If the inspection uncovers significant issues (such as structural damage, electrical problems, or a failing roof), the buyer can:

- Request repairs or credits from the seller

- Renegotiate the purchase price

- Cancel the contract and recover their earnest money deposit

Why Is It Important?

This contingency protects buyers from being locked into a contract for a home with hidden defects or costly repairs. It also gives sellers the opportunity to address any problems before closing, which can help keep the deal on track.

If the inspection reveals serious flaws in the home’s condition and those flaws have been spelled out in the contract, the buyer may back out or request that the seller repair the issues or lower the purchase price.

Typical Home Inspection Process

- The buyer hires a licensed home inspector.

- The inspector evaluates the property’s condition (roof, foundation, plumbing, electrical, etc.).

- The inspection report is shared with both parties.

- The buyer decides whether to proceed, renegotiate, or withdraw.

Common Issues Found During Inspections

- Water damage or mold

- Outdated or unsafe electrical systems

- Roof leaks or damage

- Foundation cracks

- Pest infestations

If any of these issues are deal-breakers and the seller won’t fix them, the buyer can exit the contract thanks to the inspection contingency.

2. Financing (Mortgage) Contingency

What Is a Financing Contingency?

A financing or mortgage contingency makes the sale dependent on the buyer’s ability to secure a mortgage loan. If the buyer can’t get approved for financing within a specified timeframe (usually 21–30 days), they can cancel the contract without penalty.

Why Is It Important?

Most buyers need a mortgage to purchase a home. This contingency ensures that if the buyer’s loan application is denied—due to credit issues, job loss, or changes in lender requirements—they aren’t forced to buy the home or forfeit their earnest money.

A financing contingency, also known as a mortgage contingency, is an agreement that the home purchase depends on your ability to secure a mortgage. This clause is often included in the purchase agreement to ensure that if you’re unable to obtain financing, you can legally withdraw from the deal without facing financial penalties.

Typical Financing Process

- The buyer applies for a mortgage and submits required documentation.

- The lender reviews the buyer’s credit, income, and debt.

- The lender orders an appraisal to confirm the home’s value.

- If approved, the loan moves to closing; if denied, the buyer can walk away.

How It Protects Buyers

Without this contingency, a buyer who can’t get a loan might be legally obligated to complete the purchase or risk losing their earnest money deposit.

Other Common Contingencies in Real Estate

While the inspection and financing contingencies are the most common, there are several others you might encounter:

- Appraisal Contingency: Ensures the home appraises for at least the purchase price; if not, the buyer can renegotiate or exit.

- Title Contingency: Protects the buyer if there are issues with the property’s title, such as liens or ownership disputes.

- Home Sale Contingency: Makes the purchase dependent on the buyer selling their current home first.

- Homeowners Insurance Contingency: Requires the buyer to secure insurance for the property before closing.

These additional contingencies provide further protection but can also make an offer less attractive to sellers, especially in competitive markets.

How Contingencies Impact the Home Buying Process

For Buyers

Contingencies = Protection.

They allow you to move forward with confidence, knowing you can withdraw if something major goes wrong.

But…

Too many contingencies can make your offer less appealing, especially if there are multiple buyers competing for the same property. In a hot market, sellers may favor offers with fewer contingencies or those where the buyer waives certain protections.

For Sellers

Contingencies introduce uncertainty. A deal could fall through if the buyer can’t get financing or if the inspection reveals major issues. Sellers may prefer offers with fewer contingencies or may negotiate deadlines to keep the process moving.

What Happens If a Contingency Isn’t Met?

If a contingency isn’t satisfied, the contract is usually voided, and the buyer gets their earnest money back. For example:

- If the inspection reveals costly repairs and the seller won’t address them, the buyer can walk away.

- If the buyer’s mortgage application is denied, they can cancel the deal without penalty.

This flexibility is why contingencies are so valuable in real estate contracts—they provide a legal and financial safety net for both parties.

Contingency Deadlines and Negotiations

Deadlines matter.

Each contingency will have a specific timeframe—such as 10 days for inspections or 30 days for financing. Missing these deadlines can mean losing your right to withdraw based on that contingency.

Negotiation is key.

If an issue arises, buyers and sellers can often renegotiate terms instead of canceling the deal outright. For example, a seller might agree to make repairs or lower the price if the inspection uncovers problems, or the buyer might seek more time to secure financing.

Earnest Money and Contingencies

When you sign a purchase agreement, you’ll typically put down earnest money—a deposit that shows you’re serious about buying. If you back out for a reason not covered by a contingency, you could lose this deposit. But if you withdraw because a contingency isn’t met, you’ll usually get your earnest money back.

Should You Waive Contingencies?

Some buyers consider waiving one or both major contingencies to make their offer more attractive, especially in a seller’s market. However, this approach carries significant risks:

- Waiving inspection: You might end up with a home that needs expensive repairs.

- Waiving financing: You could be forced to buy a home you can’t afford if your mortgage falls through.

Always weigh the risks and consult with your real estate agent before waiving any contingencies.

Frequently Asked Questions

Do all purchase agreements include contingencies?

Not all, but most do—especially for inspection and financing. In rare cases, buyers may waive all contingencies to win a bidding war, but this is risky.

How often do contingent offers fall through?

According to the National Association of REALTORS®, only about 5% of purchase contracts fell through in the previous three months, most commonly due to inspection issues or financing problems.

Can I make an offer on a home that’s already contingent?

Yes, you can submit a backup offer. If the first deal falls through, the seller may consider your offer next.

What happens to my earnest money if a contingency isn’t met?

You typically get your earnest money back if you withdraw due to an unmet contingency.

Key Takeaways for Buyers and Sellers

- Most purchase agreements are contingent on two items: home inspection and financing.

- These contingencies protect buyers from buying a home with hidden problems or one they can’t afford.

- Sellers may prefer offers with fewer contingencies, but removing them increases risk for buyers.

- Always understand the terms and deadlines of each contingency before signing a contract.

- Consult with a real estate agent to determine which contingencies are right for your situation.

At YesLoanz.com, we’re committed to helping you navigate the home buying process with confidence. Whether you’re a first-time buyer or a seasoned investor, understanding contingencies—and how they protect your interests—is essential for a smooth, successful transaction.

Ready to take the next step?

Get pre-approved for a mortgage, connect with a trusted real estate agent, and make sure your purchase agreement includes the right contingencies for your peace of mind.

For more expert tips on home buying, financing, and real estate trends, explore our blog or reach out to our team today!

This article is for informational purposes only and does not constitute legal or financial advice. Always consult with a licensed real estate professional or attorney regarding your specific situation.

Most Purchase Agreements Are Contingent on Which Two Items? A Complete Guide for Homebuyers

If you’re searching for your dream home or preparing to sell, you’ve probably come across the word “contingent” in real estate listings or during negotiations. But what does it really mean—and, more importantly, what are the two most common contingencies in a purchase agreement? At YesLoanz.com, we’re here to demystify these essential contract terms so you can move forward with confidence.

What Does “Contingent” Mean in Real Estate?

In real estate, a contingency is a condition written into the purchase agreement that must be met for the sale to proceed. If a contingency is not satisfied, the buyer (and sometimes the seller) can walk away from the deal without penalty. Think of contingencies as legal “escape hatches” that protect both parties from unforeseen problems that could otherwise result in financial loss or legal headaches.

For example, if a buyer’s offer is accepted but a home inspection reveals major issues, the buyer can back out of the deal and keep their earnest money deposit. Similarly, if the buyer can’t secure a mortgage, they aren’t forced to complete a purchase they can’t afford.

Most Purchase Agreements Are Contingent on Which Two Items?

The two most common contingencies found in home purchase agreements are:

- Home Inspection Contingency

- Financing (Mortgage) Contingency

Let’s take a closer look at each and see why they are so important for both buyers and sellers.

1. Home Inspection Contingency

What Is a Home Inspection Contingency?

A home inspection contingency gives the buyer the right to have the property professionally inspected within a specified period—usually 7 to 14 days after the contract is signed. If the inspection uncovers significant issues (such as structural damage, electrical problems, or a failing roof), the buyer can:

- Request repairs or credits from the seller

- Renegotiate the purchase price

- Cancel the contract and recover their earnest money deposit

Why Is It Important?

This contingency protects buyers from being locked into a contract for a home with hidden defects or costly repairs. It also gives sellers the opportunity to address any problems before closing, which can help keep the deal on track.

If the inspection reveals serious flaws in the home’s condition and those flaws have been spelled out in the contract, the buyer may back out or request that the seller repair the issues or lower the purchase price.

Typical Home Inspection Process

- The buyer hires a licensed home inspector.

- The inspector evaluates the property’s condition (roof, foundation, plumbing, electrical, etc.).

- The inspection report is shared with both parties.

- The buyer decides whether to proceed, renegotiate, or withdraw.

Common Issues Found During Inspections

- Water damage or mold

- Outdated or unsafe electrical systems

- Roof leaks or damage

- Foundation cracks

- Pest infestations

If any of these issues are deal-breakers and the seller won’t fix them, the buyer can exit the contract thanks to the inspection contingency.

2. Financing (Mortgage) Contingency

What Is a Financing Contingency?

A financing or mortgage contingency makes the sale dependent on the buyer’s ability to secure a mortgage loan. If the buyer can’t get approved for financing within a specified timeframe (usually 21–30 days), they can cancel the contract without penalty.

Why Is It Important?

Most buyers need a mortgage to purchase a home. This contingency ensures that if the buyer’s loan application is denied—due to credit issues, job loss, or changes in lender requirements—they aren’t forced to buy the home or forfeit their earnest money.

A financing contingency, also known as a mortgage contingency, is an agreement that the home purchase depends on your ability to secure a mortgage. This clause is often included in the purchase agreement to ensure that if you’re unable to obtain financing, you can legally withdraw from the deal without facing financial penalties.

Typical Financing Process

- The buyer applies for a mortgage and submits required documentation.

- The lender reviews the buyer’s credit, income, and debt.

- The lender orders an appraisal to confirm the home’s value.

- If approved, the loan moves to closing; if denied, the buyer can walk away.

How It Protects Buyers

Without this contingency, a buyer who can’t get a loan might be legally obligated to complete the purchase or risk losing their earnest money deposit.

Other Common Contingencies in Real Estate

While the inspection and financing contingencies are the most common, there are several others you might encounter:

- Appraisal Contingency: Ensures the home appraises for at least the purchase price; if not, the buyer can renegotiate or exit.

- Title Contingency: Protects the buyer if there are issues with the property’s title, such as liens or ownership disputes.

- Home Sale Contingency: Makes the purchase dependent on the buyer selling their current home first.

- Homeowners Insurance Contingency: Requires the buyer to secure insurance for the property before closing.

These additional contingencies provide further protection but can also make an offer less attractive to sellers, especially in competitive markets.

How Contingencies Impact the Home Buying Process

For Buyers

Contingencies = Protection.

They allow you to move forward with confidence, knowing you can withdraw if something major goes wrong.

But…

Too many contingencies can make your offer less appealing, especially if there are multiple buyers competing for the same property. In a hot market, sellers may favor offers with fewer contingencies or those where the buyer waives certain protections.

For Sellers

Contingencies introduce uncertainty. A deal could fall through if the buyer can’t get financing or if the inspection reveals major issues. Sellers may prefer offers with fewer contingencies or may negotiate deadlines to keep the process moving.

What Happens If a Contingency Isn’t Met?

If a contingency isn’t satisfied, the contract is usually voided, and the buyer gets their earnest money back. For example:

- If the inspection reveals costly repairs and the seller won’t address them, the buyer can walk away.

- If the buyer’s mortgage application is denied, they can cancel the deal without penalty.

This flexibility is why contingencies are so valuable in real estate contracts—they provide a legal and financial safety net for both parties.

Contingency Deadlines and Negotiations

Deadlines matter.

Each contingency will have a specific timeframe—such as 10 days for inspections or 30 days for financing. Missing these deadlines can mean losing your right to withdraw based on that contingency.

Negotiation is key.

If an issue arises, buyers and sellers can often renegotiate terms instead of canceling the deal outright. For example, a seller might agree to make repairs or lower the price if the inspection uncovers problems, or the buyer might seek more time to secure financing.

Earnest Money and Contingencies

When you sign a purchase agreement, you’ll typically put down earnest money—a deposit that shows you’re serious about buying. If you back out for a reason not covered by a contingency, you could lose this deposit. But if you withdraw because a contingency isn’t met, you’ll usually get your earnest money back.

Should You Waive Contingencies?

Some buyers consider waiving one or both major contingencies to make their offer more attractive, especially in a seller’s market. However, this approach carries significant risks:

- Waiving inspection: You might end up with a home that needs expensive repairs.

- Waiving financing: You could be forced to buy a home you can’t afford if your mortgage falls through.

Always weigh the risks and consult with your real estate agent before waiving any contingencies.

Frequently Asked Questions

Do all purchase agreements include contingencies?

Not all, but most do—especially for inspection and financing. In rare cases, buyers may waive all contingencies to win a bidding war, but this is risky.

How often do contingent offers fall through?

According to the National Association of REALTORS®, only about 5% of purchase contracts fell through in the previous three months, most commonly due to inspection issues or financing problems.

Can I make an offer on a home that’s already contingent?

Yes, you can submit a backup offer. If the first deal falls through, the seller may consider your offer next.

What happens to my earnest money if a contingency isn’t met?

You typically get your earnest money back if you withdraw due to an unmet contingency.

Key Takeaways for Buyers and Sellers

- Most purchase agreements are contingent on two items: home inspection and financing.

- These contingencies protect buyers from buying a home with hidden problems or one they can’t afford.

- Sellers may prefer offers with fewer contingencies, but removing them increases risk for buyers.

- Always understand the terms and deadlines of each contingency before signing a contract.

- Consult with a real estate agent to determine which contingencies are right for your situation.

At YesLoanz.com, we’re committed to helping you navigate the home buying process with confidence. Whether you’re a first-time buyer or a seasoned investor, understanding contingencies—and how they protect your interests—is essential for a smooth, successful transaction.

Ready to take the next step?

Get pre-approved for a mortgage, connect with a trusted real estate agent, and make sure your purchase agreement includes the right contingencies for your peace of mind.

For more expert tips on home buying, financing, and real estate trends, explore our blog or reach out to our team today!

This article is for informational purposes only and does not constitute legal or financial advice. Always consult with a licensed real estate professional or attorney regarding your specific situation.